Across the United States, the renewable energy policy landscape varies as much as the terrain. Solar and wind policies are driven largely by individual states—each with its own focus (or lack thereof).

Following are highlights of the most-promising and least-promising states according to their current renewable energy policies, and a look at trends for the current U.S. energy policy.

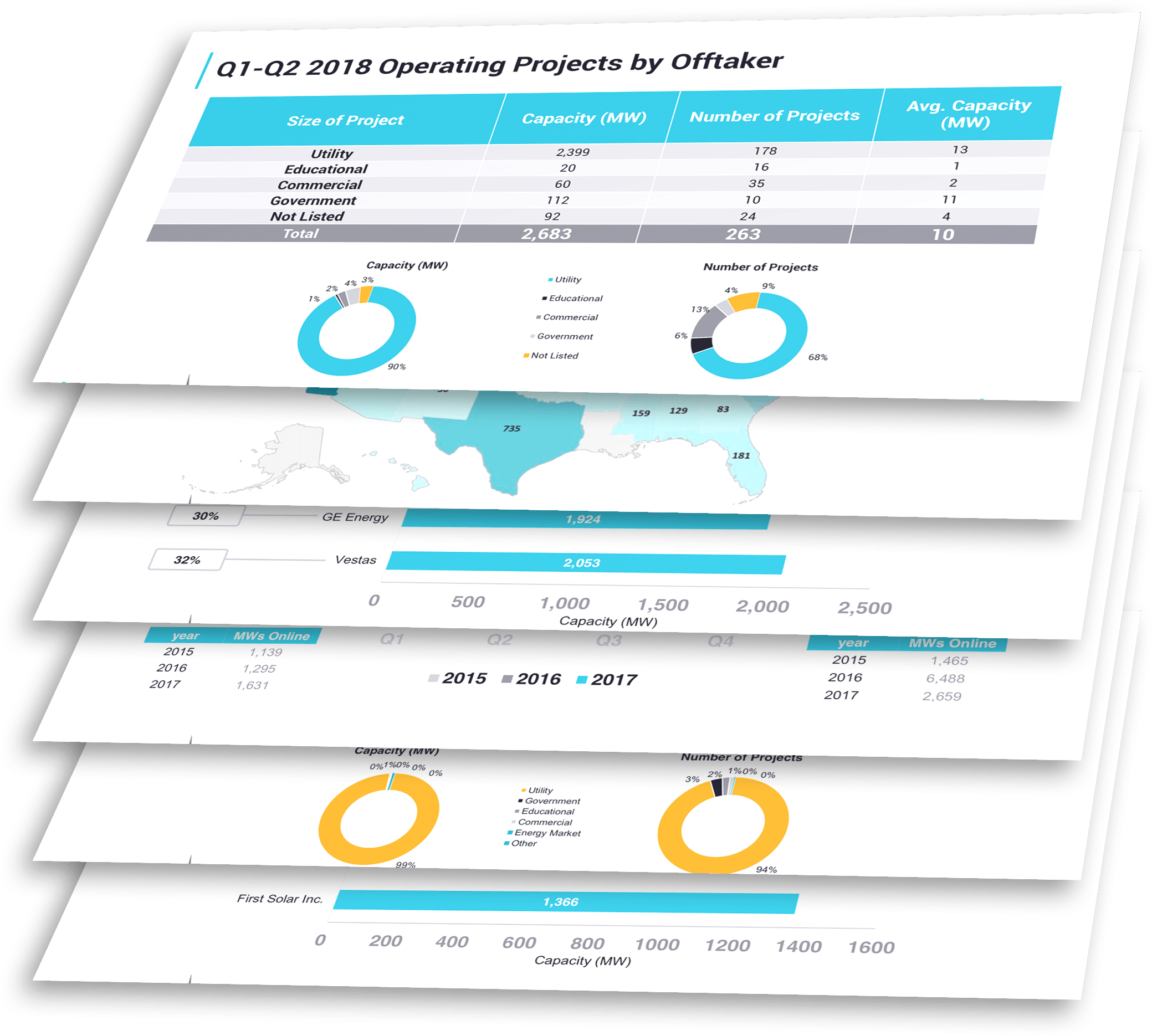

Source: Energy Acuity Renewables Platform

States That Look Promising For Renewable Energy

Oregon

Oregon’s energy landscape is changing. Long home to a diverse energy portfolio, the state legislature, and public utility commission have demonstrated a strong desire to increase solar generation. More than 60 MW of solar came online in 2016, nearly doubling the state’s solar capacity. For 2017 that increase looks poised to continue; however, growth will be largely dependent on legislation.

Connecticut

At times overshadowed by its neighbors to the north and west, Connecticut has historically received less attention from renewable energy developers than states like New York and Massachusetts. This is quickly changing thanks to a robust portfolio of solar-friendly policies—Connecticut is one of the fastest-growing solar markets. Existing Connecticut solar policy includes an RPS requiring 27% clean energy production by 2020, which includes solar carve-out (300 MW residential by 2023).

Rhode Island

Rhode Island, perhaps hoping to improve its notoriously poor business climate, appears to have taken cues from neighboring Connecticut and is developing a decidedly pro-renewable energy policy environment. 2016 was a banner year for solar policy in Rhode Island, but the legislative support for solar is by no means satisfied. Rhode Island solar policy is considered “open for growth”—the doubling of Rhode Island’s RES sends a clear message to developers, utilities, and energy consumers.

States With A Longer Way To Go

Florida

The Sunshine State? Maybe not as much as you’d think. Overwhelmingly outperformed by regional neighbors like North Carolina and Georgia, Florida has recently sought to encourage the growth of its solar industries.

Unfortunately, policy developments have, for the most part, removed only the most basic barriers to entry for solar developers in Florida. 2016 was a contentious year for solar policy in Florida, but solar interests prevailed. 2017 legislation is building on that momentum, with several legislative bills that will bring solar energy closer to the forefront. Small-scale solar growth is at least possible in Florida as primary barriers to entry are removed.

South Carolina

Like Florida, South Carolina has tremendous solar potential but is just now beginning to form a solar energy policy that will encourage growth. South Carolina lacks the overarching policy support provided by a robust RPS, but recent legislation has slowly and steadily supported solar growth. 2017 legislation appears to be following suit.

South Carolina’s policy movements in support of solar will surely encourage growth, but without more significant utility-driven procurement, property tax relief alone may fail to induce the renewable energy boom seen in neighboring North Carolina and Georgia.

Nebraska

With the exception of its robust biofuel industry, Nebraska is not known for RE development. Nebraska does not have an RPS and is the only state in the nation to receive all of its electricity from publicly owned utilities, which at times have struggled to support development in ways investor-owned utilities have not.

And the state is clearly missing an opportunity: In 2016, Nebraska ranked 13th nationally in solar potential, but 47th in installed capacity; similarly the state ranked fourth nationally in wind potential, but 20th in installed capacity.

2016’s legislative session opened new avenues for industry growth through deregulation and increased financing mechanisms for solar policy and wind policy. This should encourage the deployment of residential and commercial rooftop solar, C-BED, and utility-scale wind.

It remains to be seen what will come of this year’s legislative session, though it’s clear lawmakers are keen to capitalize on renewable energy’s momentum.

Trends For U.S. Renewable Energy In 2017/ Federal Overview

The federal climate for renewables is currently getting mixed messages. As the Trump administration works to terminate the Clean Power Plan, the market is going to be decided by a combination of cost and consumer demand. With cheap natural gas, the shift back to coal production is very unlikely; with renewable energy costs continuing to drop, wind and solar energy are competing on a dollar-per-dollar basis. Residential and commercial consumers’ appetites for renewable energy are at an all-time high as more companies introduce sustainability programs.

Want to know more?

To learn more about wind energy and solar energy policies and projects in these states and throughout the country, check out the full version of the project profiles in the Energy Acuity Renewables Database.

Source: Energy Acuity

Need Detailed Renewable Energy Intelligence & Analysis? Request a Free Demo of the Energy Acuity Platform Today!

Energy Acuity (EA) is the leading provider of power generation and power delivery market intelligence. EA’s unique approach merges primary research, public resource aggregation, web monitoring and expert analysis that is delivered through a simple, dynamic online platform. This allows our clients to focus on actionable information and win business over the competition.