The North American power industry is facing an unprecedented challenge: How to absorb thousands of megawatts of renewable-sourced power, a growing amount of which is on the “wrong side” of the utility meter, into the everyday reality of power consumption. This massive block of capacity and the speed with which renewables are entering the market is causing a massive dislocation of not only conventional resources but the very infrastructure on which these resources have functioned for decades. Low-cost power, battery technologies, artificial intelligence guiding systems and a range of alternative infrastructure investments are factors that are reshaping power economics. While this may seem like a problem far removed from day-to-day utility operations, these are the forces that are shaping the future for utilities and throwing their heretofore safe model of regulated rate of return, and how they do business, into chaos. This dislocation is what will be defined as the challenge of the 21st century and the “Renewable Century” is now an indisputable reality. The size, scope, and speed of this reality is catching many people in the industry off-guard.

Speed Kills

It is the speed that new renewable power generation assets are flooding the market that is creating an unprecedented challenge and dislocation. This dislocation, mainly of conventional assets, but extending to transmission and distribution assets as well, is reshaping the way power is generated and distributed, and it is this extension that is affecting utilities more than other market participants. Technologies, specifically alternative infrastructure technologies (AIT), or non-wires alternatives, are those that look to work on understanding the intersection of power generation and consumption in the aggregate. AITs are things that allow a great range of control and analysis of things like, distributed solar battery systems, micro-grids, vehicle electrification, demand response with variable diurnal load, and monitoring how much power is available across the grid. To further complicate matters for utilities is the fact that, despite rhetoric, most utilities are slow to act and continue to live in the past. Many feel they can just wait, or talk a lot about programs for carbon neutrality in 2040 or 2050, or lobby hard against renewables to reshape things like Public Utilities Regulatory Policies Act (PURPA), or buy the technology at pennies on the dollar because cash-strapped tech entrepreneurs will do anything to sell into the utility ecosystem. Their narratives need to be refreshed and there is a definite need to help them rethink the traditional utility/customer relationship and the role utilities might play in the new power ecosystem.

“It is the sheer size and speed of the renewables change that has caught many people in the electric power industry unaware.”

Tides have changed

The electric power industry has faced mega-challenges before. Some of the more significant challenges being: deregulation in the late 1990’s, rise of gas power generation in the mid 2000’s, electricity demand destruction after the 2008 financial collapse, and coal/gas switching 2009-present. Each of these events came with dislocation as the norm and there were winners and losers. While fortunes were made and lost, utilities faired reasonably well throughout managing to acquire, or divest, or lobby their way out of any potential trouble. That because the structure of the central thermal plant and wires was little changed.

Things are very different now. It is the sheer size and speed of the renewables change that has caught many people in the electric power industry unaware. For the renewable power focused industry now is a great and exciting time. Developers, manufacturers and suppliers of renewable power generating kit and their supporting companies are having a field day. This comes at the expense of conventional thermal assets which lack the economic staying power to keep up with zero variable cost power production.

Furthermore, it is reality that wind and solar assets have lower Levelized Cost of Energy (LCOE), the all-in cost of investment and technology, than many traditional thermal and hydroelectric assets. See figure 1. Stack subsidies on top of renewable LCOE and its ‘lights out’ for many traditional thermal assets. That’s tough news for those utilities that have billions of dollars of investment stuck in these thermal assets and their connected infrastructure. Tough because they apply year-on-year to have these traditional dinosaurs of generation included in the regulated asset rate base. It is just a matter of time before public utilities commissions’ re-assess the value of these assets and yield to increasing pressures to force underperforming assets outside of the traditional rate base.

Figure 1 Levelized Cost of Energy – $/MWh basis- including debt, interest payments, and equity. Source: Lazard

If the speed of change is our first issue, and economics our second, then issue three is the clump of renewable assets entering the market and the position of this clump. This clump is fraying the traditional one-way relationship of utility supply and customer demand. Markets are no longer source to load/sink (wholesale supply/retail demand). In fact, many markets may now be characterized as source to source even if that is confusing. Consider that solar asset deployment often means power is being generated behind the utility’s meter (BTM) and that power may be directly attached to the load or sink. Yet in times of generation excess BTM power is able to access the larger in-front of the meter (iFoTM) grid. This is causing indigestion for the utility world in the US.

“Comir, Comir, Comir. I think I’m gonna be sick!” [1]

While utilities are driving much of the demand for larger-scale wind and solar assets, demand for smaller-scale wind and solar assets and solar/battery and other energy storage combinations is being driven by different forces.

Commercial, Industrial and Residential (COMIR) demand for solar power is buoyed by demand for cheap and clean power, autonomy in generation, and self-determined security of supply. In addition to these factors, favorable state policies, renewable portfolio standards, clean power regulations and desire for off-grid and micro-grid solutions are driving many COMIR customers to seek self-determination; their control over the power they consume. While utilities still have a role to play in providing power to their rate-base, their traditional role of power supplier is being tested, and in cases, replaced faster than they or their public utilities commission’s regulations can keep up.

“It is just a matter of time before public utilities commissions re-assess the value of these assets and yield to increasing pressures to force underperforming assets outside of the traditional rate base.”

This replacement is coming from COMIR self-determination. COMIR consumers recognize that wind power, solar resources and solar battery combinations can give them flexibility in how they satisfy their desire for clean, cheap and reliable power. While utilities continue to measure customer satisfaction and other customer measures they do so out of ‘fealty’ to their public utility commission overlords, rather than a true desire to satisfy consumer need. If consumer need was the priority, one could argue, there would be a greater range of product options for consumers. Customer satisfaction at the utility generally revolves around how quickly power is restored after an outage and how consumers feel about their utility’s brand, rather than quality of the service or other measures like flexible rate pricing.

Customer Experience/satisfaction is one measure that helps utilities support a higher regulated rate of return in their rate case filings. Utilities still look to fight the age-old regulatory fight while their customers are seeking a way to cut the cord and find cheaper, more sustainable and cleaner power. Many utilities are encumbered with crushing pension plans, a hangover from when companies actually set aside funds for their employee’s retirements. For example, Southern Companies’ current pension liability is $13 billion (year-end 2018), on revenues of $23 billion. It’s no wonder that regulators, utilities and politicians seek to maintain the status quo. Consider that some 14% to 17% of most Americans’ 401(k)s/Individual Retirement Accounts (IRAs) and a significant proportion of pension fund investments are made up of investor owned utilities (IOUs) stocks and this total utility industry exposure perhaps swings higher when utility bonds are considered. It’s a tonne of cash. Actually, its many hundreds of tonnes or billions of dollars making up this investment. Make a change to how IOUs are generating revenues and how they receive regulated returns and that impacts their finances which, in turn, messes with a lot of market value.

Utilities need to understand that much of their future capital spend will have to change from investing in the traditional ‘rate-baseable’ assets, the large centralized power plants and supporting transmission infrastructure of the past, to a focus on local-scale congestion management, grid rectification, voltage support of the low voltage distribution network, and working out how to deal with a surge in power generation at traditional demand sinks that will require a distribution grid capable of absorbing bi-directional power flows at the 12.5 kV level.

Put a solar system on a roof and you create a need for the consumer to interact with their utility. Put solar systems on a million roofs and it’s the utility that needs to interact with the consumer. A million solar installations can inject as much as 5.4 GW of power right where it is needed, save for the fact that electricity demand peaks during the day. Battery systems further complicate economics. Controlling this oscillating power source is challenging. This dislocation, like global warming and climate change, is happening faster than the mainstream perceive or want to perceive.

“While utilities continue to measure customer satisfaction and other customer measures they do so out of ‘fealty’ to their public utility commission overlords, rather than a true desire to satisfy consumer needs.”

It is this perception that will either keep the utility industry moving forward or will reinforce the status quo and see utilities fall behind. For utilities, they need to decide if they are to be truly proactive or whether they maintain their reactive status quo. Reactive status quo is a good driver of current regulatory policy that is intended to support the age-old utility monopoly rather than support fresh market structures. When policy does look to solve issues, it is usually to tackle large issues like, market reforms, reliability, and/or how to support generators and their compensation when market pricing is being driven to lower and lower levels by renewable power.

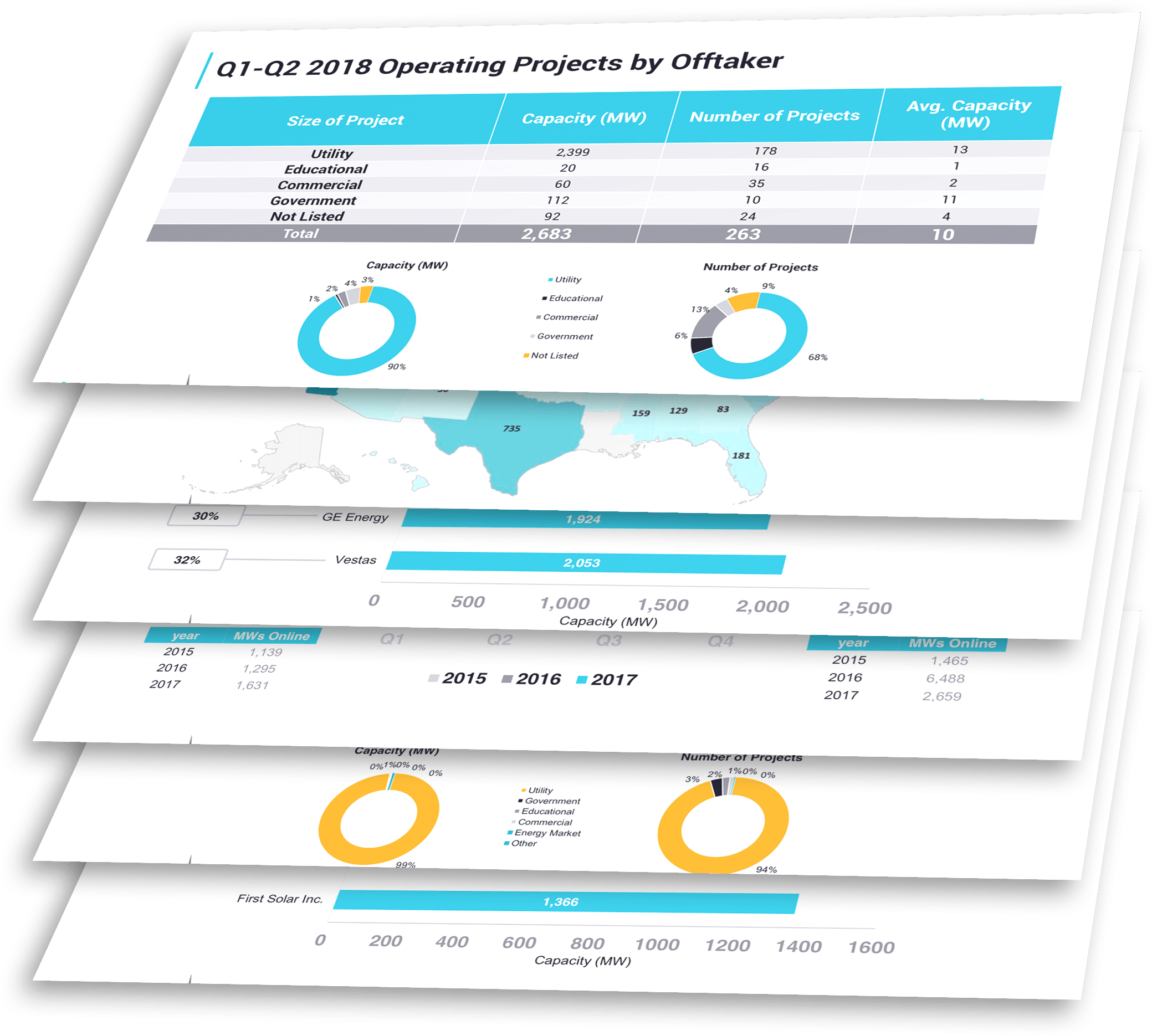

To be proactive, utilities and their advisors need to understand the combination of fundamental market data and information, and comprehensive analysis of the factors impacting utility networks and decisions. It is here where there is even dislocation in keeping track of the market, its data, its information and analysis, itself. Many utilities and their advisors rely on market data from the conventional power space and from consultants looking to support and maintain the utilities status quo, rather than dig into the new reality of the industry. For example, the Energy Information Administration’s, a US government department focused on the US Energy sector, Q3 2019 forecast suggests 104,000 MWs of total new build capacity (of all types; i.e. nat gas 43GW, wind and solar 53GW) coming into the market over the next decade. Energy Acuity, a Denver Colorado-based, leading energy information analysis firm, is tracking a staggering 230,000+MWs of wind capacity and 291,000+ MWs of solar capacity and 63,000MWs of natural gas capacity over the same period. For contrast this 0.5 TW of new renewable build represents a little over 40% of the current 1.2 TW of generation capacity that is in service to meet US peak demand of about 0.7 TWs. Granted not all of this capacity is going to be built, but it represents the size of the issue facing the space.

This amount of capacity coverage from EA, when compared to the EIA or other industry data provider’s offerings represents a potential major disconnection. Companies relying on outdated, incomplete or inaccurate data sources stand to skew their analysis against this raft of capacity. This will, no doubt, lead their strategic planning to tackle a different reality. It’s the old garbage-in, garbage-out adage that has plagued the electric power space since Tesla and Edison were messing around. Consider that if just half or even a quarter of this capacity is built, 250,000 MW, 125,000 MW (0.25 Terawatts (TW), 0.125TW) it still represents the type of dislocation the industry is wholly unprepared to tackle.

The energy industry’s analysis has always been about capacity and the changing value of capacity. The bow wave of tectonic shift pulsing through the electric power industry is reshaping not only the mix of generation, but the connection of power sources to the market and it is blurring the lines between the wholesale and retail sectors. Continued downward pressure on power prices through renewable power sources is giving COMIR customers the signal that they can make their own power at a fraction of the utility rate. Downward pressure on prices in turn scuffs out the economics on convention power generation making these assets’ value lower. Utilities need to understand the impact of changing market fundamentals, of changing state and federal policy, and the impact of alternative technologies on their existing infrastructure. That knowledge will allow them to be a part of the generation future and how to engage with their customers or be relegated to a role of marginal rent collectors as the value of their assets’ diminishes over time.

About The Author

Michael is the Chief Revenue Officer at Energy Acuity, LLC based in Denver, Colorado. Prior to Energy Acuity, LLC Michael was CRO at EPIS/Energy Exemplar. Michael was head of SNL Energy, the energy division of SNL Financial until its sale to S&P Global in 2015. He joined SNL in 2009 from Duff and Phelps LLC, where he was the Director of their Energy Advisory and Consulting practice. Prior to this, he was the Senior Director of Product & Business Development for Platts, a division of The McGraw-Hill Companies. Michael has more than 25 years’ experience in the electric power, energy, mining and utilities industries, analyzing assets, companies and industry issues. Michael is a graduate of Canberra College of TAFE, the Australian National University, and the Colorado School of Mines.

Additional Reading:

[1] Alexei Sayle, The Young Ones, BBC Two 1982-1985, bbc.com.uk